Thinking about growing your wealth through property is always the very first step in the process. Entertaining the thought, and wondering if it is possible, however seeing your dreams and goals come to fruition will always require planning, and working with specialists that support that dream and goal. While the property and the related benefits may be the bigger picture goal, The logistics need to be considered, such as where the deposit will come from (equity, or savings?), and what needs to occur in order to pass the bank's loan assessment, in order to obtain the finance. So, with lots of moving parts, and elements to understand, best you get into the driver's seat with having us look at what you need to do in order to occur your dreams! So, some steps, to get you thinking! Step 1: Speak with a Mortgage Broker When considering an investment property, your first port of call should always be your mortgage broker. We will review your assets and liabilities to determine how much you can borrow, which will, in turn, give you a general idea of your target price range, so you can narrow your property search within your purchase budget. Step 2: Budgeting Just like buying your first home, when purchasing an investment property, it’s essential to budget. If you’re unsure of the best way to budget for an investment property, speak with your mortgage broker to help you to get on the right path. Step 3: Important conversations Your broker will discuss your plans and your circumstances with you to determine what you can afford. Your broker will also provide statutory documentation to initiate the lending process and discuss with you what loan products will be appropriate to your specific circumstances, based on your goals and objectives. Want to know more? There is so much to know, and understand.... want to get into the drivers seat and take control of your financial future? Let's have a chat to find out more!  Amidst the roller coaster ride of 2020, we reached a silver lining. The Australian government announced HomeBuilder: a $700M housing package for Australians to access $25k grants for building a new home or substantially renovate an existing home. This is available to eligible owner-occupiers including first home buyers and is a time-limited, tax-free grant program to help the residential construction market to get through the Coronavirus pandemic by encouraging the building of a new home and renovations this year. HomeBuilder is available for building contracts signed between 4 June 2020 and 31 December 2020, where construction or renovation commences within three months of the contract date. Owner-occupiers must meet the following eligibility criteria:

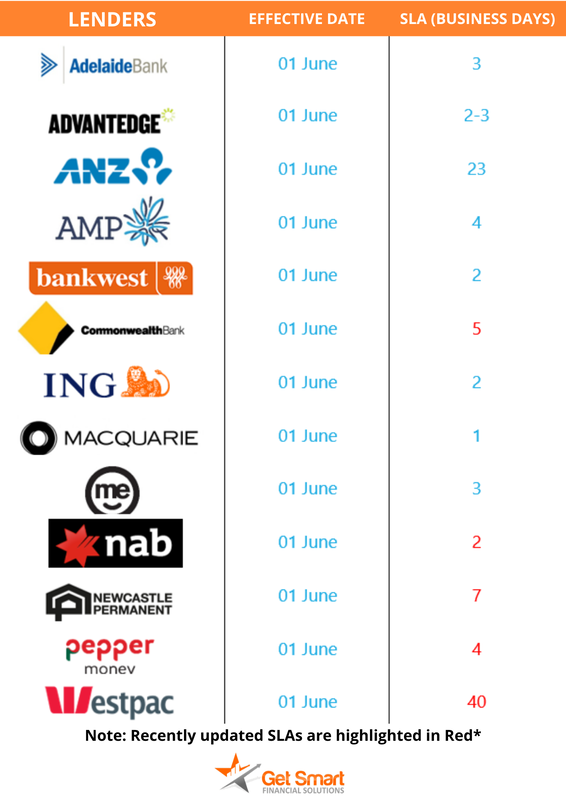

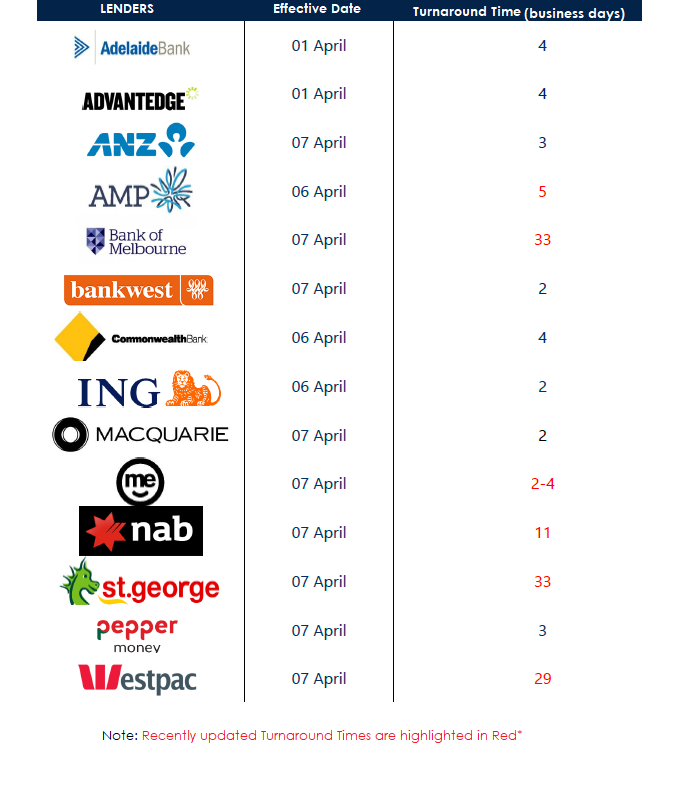

If you want to know if you meet the eligibility requirements or just want to know more about the HomeBuilder grant, book a Zoom meeting for us to discuss! With the rapid increase in the number of mortgage lenders offering home loans to consumers, the process is even more complicated than in years past. Fortunately, Get Smart Financial is here to help. We have regular contact with a wide variety of lenders, some of whom you may not even know about. Working with us can save you time! Purchasing a property can be a life-changing experience but the home loan application process can be really daunting if you’re new to the process. We can prepare your application on your behalf and mitigate the risks in your request. See below banks for the current turnaround times.  If you have any questions, book in a time with me below.  How debt impacts your home loan application

Almost everyone has a debt of some sort - whether it be paying off a student loan (HECS or HELP debt), tax debt, credit cards, personal loans, car loans, or an existing home loan. These debts can affect your proposed home loan application not only impacting your borrowing capacity, but also what type of product you are offered by the bank, depending on your repayment history. A lender will factor in your need to continue to service or meet this regular repayment obligation, in assessing your borrowing capacity or to determine your ability to service a new loan. Further, your repayment history on your existing debts plus the number of times you've applied for credit will affect your credit score. Your credit score will be a guide for lenders to examine how responsible you are with money and to qualify for a home loan. If you have a lot of unsecured credit, then this can be interpreted by a bank as a potential that the client is living beyond their means, and care must be taken to ensure that this discussion is managed carefully. Often we will see clients having taken up a number of credit cards, to take advantage of Award point offers for travel redemption or the like, without understanding the potential implication to their Credit Score or borrowing capacity. Personal loans Whether secured or unsecured, a bank or lender will consider repayments you have to make on personal loans. Same with home loans, they may factor in a buffer on your monthly repayments to stress test the repayment, should the interest rate change. Student loans Any outstanding debt like HECS debt may affect your loan application because it impacts the amount of money coming into your account each month. If you happen to have one, you'll need to start repaying HECS debt once your income reaches a certain threshold that's currently $45,881 a year, and the repayment is based on a percentage of your earnings, depending on what your annual gross earnings are. You can find out more about HECS debt repayment obligations here. Existing mortgage or home loan The first thing a lender will want to know is whether you plan on keeping that existing loan or discharging it. If you plan to discharge the loan, the lender will not factor in the cost of those repayments each month in assessing you for your proposed new loan. If you plan on keeping your existing loan, the bank will factor your need to keep paying the loan into your calculated borrowing capacity - this may or may not impact your application. The lender will also include your ability to service any loans over your investment properties (and include a proportion of the rental income you receive, as well as some tax benefits). Car loans A lender will factor in your car loan repayments. Even if you took out that loan with another person, a lender may treat the debt as it's entirely yours thus reducing your borrowing capacity, or they may split the loan proportionately, depending on that specific bank’s policy around the same. If you have a novated lease over your vehicle, it will likely come out of your pre-tax and possibly also your post-tax income and reduce the amount of money in your pocket each month. This would also need to be considered as an ongoing liability. As a general rule, if you have a car loan of $30,000, then it is likely that this monthly obligation will reduce your borrowing capacity for lending for residential purposes, by approximately $150,000. Careful discussion should be taken before applying for vehicle finance, and considered within the scope of what you are looking to achieve within property and property lending for the coming 5 years, given the potential implications. It is imperative you speak with a finance specialist to ensure that you are planning and mitigating any potential issues. Credit cards have a major impact on your home loan Lenders are less interested in how much you owe, and rather more focused on how much you can possibly owe! They're generally more interested in the credit limits than your credit card balance. The best practice for this is to consolidate your debts or reduce multiple credit cards. Consider closing some cards down, reducing the credit limit of any cards you keep, or consolidate your debts into your new home loan. It is notable that most banks will assume that your monthly repayment to a credit card, is between 3% and 4% of the limit of the card. If you have a credit card with a limit of $20,000 and the bank assumes a 3.5% repayment obligation if you were to max out that facility, then the monthly repayment could be around $700 per month. $700 per month, is equal to around $100,000 in residential finance borrowing capacity, so credit card limits can have a major impact on your borrowing capacity. Building your Credit Score Over the years, I have had so many discussions with clients, who think they should apply for a credit card, a personal loan, or a car loan, to build a credit score, but the complete opposite is true and this is an Urban Myth! For every application for unsecured credit or finance, your credit score is diminished, not improved. So, before you apply for credit to build a credit history, please speak with us. The truth is, you are far better off to put your effort into creating a savings history instead. Last but not least… A lender will always look at your income, your ability to service a loan, and your credit score. Any other loans could affect all three. Before applying for a home loan, make sure you talk to us, so that we can support and guide you towards planning and achieving the outcomes you want and need! Let's have a chat to discuss options on how we can help you save more!  Rate remains at record low after implementing the extraordinary mid-month rate cut in March 2020.

The Reserve Bank of Australia has left the official cash rate untouched for this month remaining at the record low rate of 0.25% as the bank commits to monitoring the state of the Australian economy. Home owners possible cash grants Most economic policies of the Federal Government are being reviewed including the possibility of cash grants to home-owners and first home-buyers. These grants are designed to prop up the businesses of tradespeople and help the building and housing construction industry. This week, the government’s fourth stimulus package is expected to be signed off by the national cabinet’s expenditure review committee. Here’s the expected conditions:

The full details will be announced in the coming week. Once we know the specifics, feel free to call us about any questions you may have. If you need further information or assistance, you can book a zoom meeting with me. With the rapid increase in the number of mortgage lenders offering home loans to consumers, the process is even more complicated than in years past. Fortunately, Get Smart Financial is here to help. We have regular contact with a wide variety of lenders, some of whom you may not even know about. Working with us can save you time! Purchasing a property can be a life-changing experience but the home loan application process can be really daunting if you’re new to the process. We can prepare your application on your behalf and mitigate the risks in your request. See below banks for the current turnaround times.  If you have any questions, book in a time with me below.

If you're a homeowner with a mortgage, for sure you came across the term 'refinancing'. Refinancing allows you to merge your debts and pay your mortgage quickly. It includes reviewing your current mortgage and swapping your loan to another lender that can better meet your needs and wants depending on your circumstance. You should consider refinancing if you want to access your equity in the property without having to sell it, like making home renovations or buying an investment property. You may also consider refinancing if another provider has a more competitive offer than your current provider. Refinancing allows you to also potentially access equity - the amount you'd get from selling your home after settling the loan, such as a mortgage on the property and other costs associated with the property. There are tons of factors you need to consider when thinking of refinancing your loan. We can help you to assess your needs and goals and your financial situation towards finding a suitable, and customized solution. How will you know if refinancing is the right option for you? It's best to speak with us about your specific needs so we can assist to determine whether you can afford a modified loan structure or change your mortgage, especially if you have more than one property. Are you looking to pay less interest? Some are skilled researchers and want to take advantage of lower interest rates other lenders to reduce repayments. This can potentially save you a lot of money in the long term and is worth reviewing on a regular basis. Saving money is one of the biggest benefits of refinancing. However, it can be complex and careful consideration is required to make sure that the benefits are not just short term, but long term gains also. We always review all loan options and figure out whether it's the right decision for you to refinance. If it's going to save you higher than $1,000 a year, then refinancing might be the best strategy. Sometimes clients can save as much as $5000 or $6000 per year! Is it ideal to change your loan type? It is essential to factor in some charges in refinancing, including to pay Lender's Mortgage Insurance (LMI) to your new lender and incur exit fees on your existing home loan. If you're thinking of refinancing, working with us gives you more negotiation power given we have over 30 lenders on panel to use in our negotiations rather than negotiating directly with one bank. We have access to loan options from a range of different lenders that you can consider, the options seem endless! Have your circumstances changed? If you encounter major life changes recently, such as a change in marital status or loss of income, you might be looking to refinance. In this instance, we can help you look for other options to consolidate your personal loans and credit cards into one loan. With this, you can lower your monthly repayments and save you interest in the long-term. Get Smart Financial can help you manage your finances. Book a time to discuss options on how we can help you save more! Follow us on our Socials Channels!  You can make a huge difference by spending less, but this is not always as easy as it sounds. An effective way to save is to reduce expenses, but you have a plan and have goals that drive you and keep you accountable (check in with them regularly to track your progress and celebrate your milestones!) Here are top tips to cut your expenses and boost your savings! Understand your spending With all the cashless payments and credit cards, it’s extremely easy to lose track of how you’re spending money. Next thing you know, you spent it all on less important things. A lot of online banking systems include tools to classify debit and make a budget, so make use of them! If not, you can download an app that helps you track your expenses. Be practical with your essentials Fundamental costs can't be avoided, however, they can be reduced. Here are a few examples:

Make sure you pay off debts or credit cards on time to avoid paying interest. Overspending Set a weekly or monthly limit on less important things, you still need to have a little fun! It will be unrealistic to cut expenses if you spend too much on buying clothes, going out, or expensive hobbies. Reduce the limit over time once you get to manage to stay within the limit. According to a survey, more than 1,000 Australians showed that 73% have a problem with overspending, mostly during Christmas and on holidays. To reduce expenses on Christmas, make a list and buy planned items within your allocated budget - make sure to not go overboard, and plan during the year for these expensive periods…. We suggest putting away an amount every week or fortnight to a gifts account, which may only be $20-$40, but at the end of the year, you will have $1000 in your gift account, so you don’t blow your big picture goals and budget! On holidays, pre-plan your trip then set a daily budget. Try your best to stick to it. Reduce costs Go over your expenses on a monthly basis and look for areas to eliminate costs. Track your spending and update your plan if you keep paying for excess or downgrade if you don't use it as much and cancel unused services. You should ask yourself: Are you getting value from your subscriptions? Are you using that gym membership? Is this necessary? Remember, if you could save more, you could buy that home, or pay off that home faster! If you need further information or assistance, let's have a chat and click on the button below! Follow us on our Social Channels! It's 2020, and while I was hoping for a little more hoverboarding aka Marty McFly, a little less pandemic, on the upside technology like Zoom is meaning that I am having a whole lot more fun! Speaking with clients about their dreams and aspirations, helping them run their lending better, and supporting them to plan for the future is actually really cool, and quite the honour and privilege! Yesterday, I had a post settlement meeting with Connie, one of my favourite clients (oh, who am I kidding, I have soooo many favourites!) for a post refinance review. We wanted to make sure that Connie and Patrick have all their banking lined up as we are expecting and have planned, renaming and customising, to ensure that their transition to Macquarie runs as smoothly as possible, and they start achieving the outcomes we set out to achieve, as quickly as possible. What was great about this, is that Connie was at home, as was I.... both working from home now, no travel time was required, nor syncing of other activities to make sure we were in the same place at the same time, and it was fun! And while I would still like to be able to arrive to meetings on my hoverboard, Zoom is not a bad alternative at all, and, there is no risk that I might fall off! Want to check in, see if we can run things a little better for you?  The Commonwealth Bank of Australia (CBA) has reminded customers that it will be automatically reducing direct debit repayment amounts for all eligible variable principal and interest (P&I) home loan customers to their minimum repayment required.

The change, which will come into effect from next Friday (1 May), is being made “given the current uncertainty surrounding coronavirus” and as part of the bank’s steps to “continue providing the financial support [CBA] home loan customers need”. As announced as part of its COVID-19 support package last month, CBA said the “one-off change” is aimed at “helping to put a little more cash in the pockets of our customers during these difficult times”, which could be then spent in the economy. Speaking last month, CEO Matt Comyn said the move could help up to 730,000 customers by reducing repayments to the minimum required under their loan contract”, and “release up to $400 per month for customers and create up to $3.6 billion in additional cash support for the economy”. Mr Comyn added: “Our home loan customers are on average 37 months ahead on their home loan repayments. Customers will be able to opt-out after the change is effective should they wish to keep their current repayments.” The bank also revealed that 39 per cent of their home loan customers are more than 12 months ahead of repayments – with the vast proportion of this being two years ahead on their mortgage. CBA said that the changes will take place between 1 and 5 May. Customers wishing to retain or change their current repayments will be able to change their direct debit repayments via the CommBank app or NetBank from 6 May. CBA added: “Please accept our reassurance that the decision was made with the best intentions, though we acknowledge that no one decision can suit everyone.” If you need further information or assistance, you can book a zoom meeting with me.  While 2020 is well and truly upon us, it is fair to say that this far in, it is absolutely going to be a year to remember, but it is not all bad, and we are seeing some great outcomes for clients in these challenging times.

The way we are doing business and interacting with clients, has changed dramatically, and for the better, despite the way that the change has evolved and become a necessity. This is Ash and Simone, some of my most lovely clients, who I must admit I am having an absolute blast working with. We did a quick catch up this morning via Zoom, which is great because no one needs to travel, if you really wanted, you could still be wearing your slippers under the desk (I would *cough* never even consider that!), and there is little downtime or planning time required, working out what time works for everyone on what particular day. And, the banks are getting with the program too, meaning that clients that are looking to purchase or finance, can do so, while still being able to social distance..... Many have quickly onboarded the ability to identify via zoom or Skype 'face to face' meetings, docusign for signing both compliance and applications, and may are now allowing loan documents to be signed via docusign for the most part. At Get Smart, we have some really handy processes in place, which make it super easy to provide both statements, data, and make bookings with the team, such as bank statements.com.au, brokerpad, and youcanbook.me, where you can book straight into our calendar, at a time and day that suits you for your zoom meeting! Thinking about your finance and want to have a chat? Need a new loan, or want to review an existing loan? Reach out, shoot us an email, give us a call, or use the link below... while 2020 is challenging, sorting your finance in 2020 has never been easier, and it could save you thousands! In the current market, we have clients looking to save money and secure home loans as fast as possible. While here at Get Smart, we are considering both what variable and fixed rate options, how much savings and refinance incentive clients can take advantage of; we are also considering turnaround times of the application process. See below banks current turnaround times, that we are factoring into our recommendations with consideration to each and every client’s particular needs!   It’s all too easy to rack up debt – credit cards, HECS, car loans – and may seem all too hard to pay it off. Debt can also have a big impact on how much money you can borrow for a home loan, so reducing your debt is essential when you set out to buy your first home.

Here are seven steps you can take towards minimising your debt and moving into the property market. 1. Work out how much you’re spending Create a spreadsheet and track your expenses for a month – record everything so you can see where your money is going. You may be spending much more than you think on some things – more than you can really afford. 2. Decide where you can cut back With a clear idea of how much you spend each month, you can figure out how much you really need to spend, and where you can cut back. That second coffee every day could be costing you $20 a week – that’s $1,000 a year. Buying your lunch rather than bringing it could cost you $2,500 a year. Buying one less bottle of wine a week could save you another $1,200 a year. With a bit of commitment, you can rein in your spending and have more money to repay debt. 3. Make a budget The only way to get on top of your credit cards is to stop using them. Make a budget for the money you need to spend each week or fortnight, based on how much money is coming in and what your necessary expenses are, and stick to it. Calculate how much is left over after you’ve paid for the necessities, then figure out how much you want for discretionary spending and how much you can put towards repaying debt. Also, put money into a contingency fund to cover unexpected expenses such as car repairs that could bust your budget and cause you to reach for the credit card. 4. Prioritise your debt Work out how much money you actually owe on credit cards and loans – you may not realise how much it is. When you know how much debt you’re in, you can think more realistically about repaying it. You need to pay at least the minimum amount due on all credit cards each month to avoid going backwards and in some cases being charged fees and penalties. But by paying only the minimum, you may never get the cards paid off; you need to pay more to make progress. Consider:

5. Make a repayment plan Armed with your budget and having worked out your debt priorities, you can plan which debts you will pay off over what period of time. Having a plan will increase your sense of control over your debt; sticking to it will increase your sense of achievement. 6. Set goals and celebrate them The thought of paying off all your debt may seem daunting, so breaking it down into milestones will help you see the way ahead. Set goals such as paying off 10%, then paying off 25% and so on. Remember to celebrate each time you reach a milestone – buy yourself lunch or go to a movie as a small reward for your achievement. 7. Stick to the plan – and ride out the setbacks Keep going with your repayment plan. If you miss a payment because of an unforeseen expense, stay positive. Avoid feeling demoralised or derailed by looking forward to the next debt milestone – you can get there.  With the current situation of the COVID-19 pandemic, at Get Smart Financial we are here to help and support clients. If you’re dealing with the impact of the COVID-19 pandemic there are practical ways your bank can help. Assistance could include; deferring loan payments, waiving fees and charges, helping with debt consolidation, etc. We we will be updating this article as need be if there are additional update from the banks to keep you informed. We have listed some bank’s relief package measures to address customers affected by Covid-19, as well as some useful links; Commonwealth Bank (CBA) Commonwealth Bank has announced a package of support for all home loan customers. This package includes the option to defer Home loan repayments for up to 6 months, with interest capitalised. In addition, you can access redraw facilities, considering a repayment holiday, reducing repayments to the minimum monthly repayment amount, or apply to change your repayments to interest only payments. Should you seek deferral of Home Loan repayment, please log on to your NetBank account or call 13 2221 6am to 10pm. For more information on CBA’s Corona Virus Relief Package, click here. Macquarie Macquarie introduced a comprehensive package of support measures to help dealing with impact of Covid-19. Immediate support measure for households & business includes the option to defer Home Loan repayments for 6 months. You can request a payment pause by completing this online form. Clients will be best served to complete and submit the application online rather than ringing due to large increase in volume to the call centre. For more information on Macquarie’s approach to Financial Assistance, click here. NAB NAB has announced a range of measures to assist businesses and homeowners. These complement the federal government and Reserve Bank of Australia’s stimulus packages. NAB Personal Customers will be able to pause home loan repayments for up to 6 months, if experiencing financial challenges, including a 3-month checkpoint. For a customer with a typical home loan of $400,000, this will mean access to an additional $11,006 over six months or $1,834/month. To talk to someone about how NAB can help, please complete the Coronavirus (Covid-19) Form, here. Westpac Westpac has supported customers, businesses and community through good and tough times and will to be there as the COVID-19 situations evolves. Westpac customers who lost their job or suffered loss of income as a result of COVID-19 you can apply for 3 months deferral on you home loan repayments with extension for a further 3 months available for review. You can apply here. Consumer customers can also request assistance by completing the Financial Hardship form. To find out more details on what support is available, click here. Heritage Bank Heritage have well-established Pandemic Management Plan in place and are actively implementing these measures. Financial Assistance Relief Package includes: 1. hardship provisions to help impacted customers 2. deferral of scheduled loan repayment 3. waiving of fees associated with restructuring of loans needed, such as switching from P&I and IO 4. waiving or refunding fees incurred due to virus impacts, for example missed payments. If you are financially impacted please reach out to Heritage as soon as possible 24/7 on 131422 Bankwest Bankwest is providing additional support to home loan customers who may be facing financial difficulty at this time with an option to defer home loan repayments for 6months. Customers with a retail home loan (regardless of income type) who may be in need of support can have their home loan repayments deferred for six months. All home loans regardless of product, purpose or repayment type can have a deferral applied. The option to defer will be available in Bankwest Online Banking under 'Self-service' > ‘Loan support'. Before starting the process, make sure contact and address details are up to date under 'My details & security'. Customers experiencing immediate financial hardship, please contact Bankwest to discuss the support options available and what they mean for individual circumstances. Customers who have variable home loan, an redraw your extra repayments using the Bankwest App or Bankwest Online Banking – here’s how or use the Home Loan Access Request Form with variable rate home loans and fixed rate home loans. Note that a minimum withdrawal amount of $1000 applies. For more information about pausing your repayments, please see our FAQs. For full information on the bank’s Coronavirus Support, click here. Bankwest contact number is 1300 134 107. ME Bank On Monday, ME announced its own package of measures to support all our customers. The announcement sparked many calls from our customers seeking more detail on what these measures are and if they are eligible for them. To help respond to customers’ enquiries about ME’s Customer Support Package, below are some more details on the options available to customers. Home Loan Repayment Holiday/Pause: The option to pause home loan repayments for up to six months, with a review at three months. How does pausing home loan work? • For home loan customers impacted by COVID-19 and the current economic uncertainty, ME has introduced a repayment pause for home loan customers. • Customers will not need to make repayments for up to six months, with a review at three months. • Interest and charges will continue to accrue during the repayment pause. What is the process to request a repayment pause? • Customers will need to contact call centre to action a repayment pause on 13 15 63 • ME will check in with the customer after 3 months to determine if the repayment pause needs to continue. If yes, will continue for another 3 months. What if a customer needs a repayment pause for longer than 6 months? • These customers will be assessed on a case by case basis by Customer Assist team. Will customers accrue interest during the pause? • Yes, interest and charges are accrued during the repayment pause. •Accrued interest will be capitalised and added to the customer’s home loan balance and repayments will be adjusted. •These future payments may be higher. This information will be helpful for customers that are not currently in hardship and are trying to understand what their options are if they go into hardship in the future. If a customer is currently in hardship, please call on 13 15 63 or fill out the form here. For more information on the bank’s Financial Hardship Assistance, click here. Bank of Melbourne (BOM) BOM have announced extensive support measures to help consumer and small business customers impacted by the outbreak of COVID-19. Customers who have lost their job or suffered loss of income as a result of COVID-19 can contact the bank for 3 months deferral on their Home Loan mortgage repayments, with extension for a further 3 months available after review. For customers who need to defer Home Loan repayments, click here. Consumer customers can also request assistance by completing the Financial Hardship Form. After filing in the form customers will receive a phone call from the bank. To find out more details on what support is available, visit the bank’s website here. Bluestone Bluestone have a range of options to support customers impacted by COVID-19. Some of these options may include:

To discuss the options available, customers can call at 13 2583 or complete the enquiry here. Virgin Money Virgin Money introduced Fast Track Hardship Assistance for customers who have been affected by Coronavirus (COVID-19), recent weather events or bushfires. The Fast Track process offers impacted customers urgent access to a range of financial relief measures, which may include:

Assistance measures will be assessed on a case-by-case basis. For customers who are impacted, may call Virgin Money on 1800 701 997. For more information on COVID-19 hardship assistance, click here. For more information on support and assistance, click here. Customers can access the emergency assistance website. Pepper Money Pepper Money customers who are impacted by the pandemic may be able to:

Alternatively, customers contact Pepper Money on 1800 356 383 8am-5:30pm Monday-Friday to discuss financial relief options. For more information on COVID-19 hardship assistance, click here. ING ING customers who have suffered a loss of income or employment due to COVID-19, can have a three-month payment pause on home loan repayments. An extension for a further three months (total 6 months) may also be available on request and is subject to financial assessment. Customers can also consider a number of different options; 1. may be able to access money available in redraw 2. might be paying down home loan with larger than required repayments. 3. can reduce repayments to the minimum monthly repayment amount. To apply for COVID-19 Hardship assistance please call on 133 464 available 8am - 8pm, 7 days a week. For more information on Financial Hardship and other repayment options available, click here. Bankfirst Bankfirst customers who are impacted by COVID-19 can call the back directly to discuss the situation on 03 9834 8530. For customers who are having difficulty making repayments, the following types of assistance may be available;

To apply for Financial Hardship Assistance, click here. For more information on the bank’s response to COVID-19, click here. Firstmac Firstmac existing hardship policy is well suited to the COVID-19 pandemic, offering; a repayment holiday for 3 months with the option to extend for a further 3 months. In response to the COVID-19 crisis, the bank assigned additional local staff to their Hardship Team so they can speak to each customer personally and will work through a solution to their individual circumstance. For customers experiencing hardship, please call on 13 12 20 and one of our Hardship Consultants will help them with consideration and empathy. Adelaide Bank Adelaide Bank announced financial assistance package for all customers affected by COVID-19, it includes;

Full information on the bank’s COVID-19 assistance, click here. Bendigo Bendigo Bank offers Financial Assistance package for customers need financial help which can include;

For customers affected by financial hardship and require a repayment release please call Mortgage Help Centre on 1300 652 146. Full information on the bank’s COVID-19 assistance, click here. AMP For AMP clients facing financial hardship as a result of COVID-19, can request to pause home loan repayments for up to three months with the option to extend for a further three months. Repayment holiday details: • A pause in home loan repayments for three months, with the option to extend for a further three months, for clients who are experiencing ongoing financial challenges as a result of COVID-19. • All home loan clients affected by COVID-19 are eligible – this includes all variable and fixed loan types, including owner occupiers and investors on both principal and interest or interest only repayment schedules and SMSF loans. • Clients who are 30+ days in arrears, or have existing hardship arrangements in place are not eligible for the repayment holiday offer, however can seek help through our normal hardship support. • During the repayment holiday, unpaid interest will be capitalised which means it will be added to the loan balance and when repayments start again they will be higher for the remainder of the loan term. During your repayment pause, unpaid interest will be capitalised which means it will be added to your loan balance and when repayments start again, they will be higher for the remainder of the loan term and may incur a higher amount of interest over the life of the loan. To start the process, enquire here or phone 13 30 30 between 8am-8pm Monday-Friday, or 9am-5pm Saturday and Sunday (AEST). For further details on financial hardship, click here. For the latest update relating to COVID-19, check out the bank’s dedicated page here. ANZ ANZ home loan customers experiencing financial difficulty due to COVID-19, may be able to support by putting home loan repayments on hold for six months, with interest capitalized. If customers pause repayments, ANZ will check after three months. It will not impact their credit rating during this period. The bank also decreased variable interest home loan rate by 0.15%pa, effective today 27 March 2020. Customers can contact ANZ Customer Connect them on 1800 252 845. For more information on the bank’s relief measures, click here. Choicelend Choicelend customers who are dealing with the growing challenges of COVID-19 may be eligible to pause their home loan repayments for a 2 to 6-month period. Choicelend is also further reducing their variable home loan rates by 0.10% p.a. for both new and existing loans, bringing the combined variable rate reduction this month (March 2020) to a total of 0.35% p.a. Other options are;

Customer can also apply for repayment pause via an online form that will be available on website within the next 48 hours. For more information on the lender’s support package, click here. Australian Finance Australian Finance have outlined contact details below for customers who might have been impacted by COVID-19. If customers are not sure which lending program they currently have with their loan, please call on 1300 888 684 or email customerservice@australianfinancial.com for assistance. For more information on specific contact for each lending program, click here. Suncorp Suncorp has announced a range of measures to assist our businesses and personal customers. These complement the federal government and Reserve Bank of Australia’s stimulus packages. Suncorp is offering lending customers impacted by COVID-19 the following on an “opt-in” basis: 1. Repayment Pause: A deferral of repayments for all home loans, for a period of up to six months (interest will be capitalised). 2. Move to Interest Only: Conversion from principal and interest repayment structure to interest only for a period of time for their home loan. 3.Cashback: Customers who have made additional repayments on their variable home loans are able to access cashback (up to the value of the advance repayments minus the value of one month’s repayment) to assist them with expenses. For fixed rate home loans, customer need to make a special request for Suncorp to grant an exception, allowing them to access cashback on their loan. 4. Modify Repayments: Customers who have made additional repayments on their home loan and are ‘in advance’ and are able to reduce or suspend their repayments (up to the value of their advance payments). Customers can apply for financial hardship and action the above options by submitting an Online Request Form. Customer Assist team will contact customers to advise the outcome of the review once complete. Customers can call Customer Care team on 13 11 55 (Monday to Friday, 8am-6pm Mon-Fri AEST). For more information on the bank’s support for COVID-19, click here. Resimac For customers who have been affected by natural disasters or COVID-19 and are concerned of their financial position, Resimac’s common type of assistance they provide include:

For Resimac-funded loan, please email financialassistance@resimac.com.au. They can help with enquiries and discuss the relief options available to customers experiencing financial hardship. For more information on the lender’ financial hardship assistance, click here. Auswide Auside is offering support to customers directly affected by COVID-19 to help ease the financial pressures caused by such events. Home loan, personal loan and business loan customers requiring financial assistance as a result of COVID-19 may have several options available to them.

To apply for financial assistance due to COVID-19 may complete the online form or call 1300 077 969. For complete details of the bank’s support and to complete the online form, click here. Beyond Bank Beyond Bank customers who are facing hardship due to loss of income or change in circumstances as a result of COVID-19 have restructuring option. Restructuring options to support home loan customers including:

For more information, click here. Citibank Citibank have a range of ways to help based customers individual circumstances, which may include things like varying the amount and frequency of repayments. For clients that has been directly impacted by COVID-19, the bank will require a clear description of how the customer has been impacted and the personal financial summary and supporting documentation will be waived. Impacts of COVID -19:

For more details on the bank’s financial hardship assistance and to how to apply click here. Alternatively call Debt Management Solutions team on 1300 300 470 from 9am-5pm, Monday - Friday (AEST) except public holidays. HomeStart Finance Homestart have programs in place to help to try and ease some financial stress on their customers. These are some of the things we may be able to offer you depending on your circumstances:

Customers who have had a change in circumstances, such as loss of employment or illness, contact the Customer Care Team on 8203 4756. Customers experiencing financial difficulty and are unsure if will be able to meet repayment obligations, contact Customer Assist Team on 8203 4081 Monday to Friday 8am – 5pm. For more information on their financial hardship assistance, click here. To follow HomeStart important update, click here. Keystart Keystart have devised a wide range of measures to assist customers who are experiencing financial hardship during these uncertain times. These include:

As the lender Is experiencing high volume of call, customers can apply for financial hardship assistance by filling out this form here. For more details on the lender’s COVID-19 support, click here. La Trobe La Trobe Financial has announced it will offer hardship assistance for small business customers who are financially affected by the spread of COVID-19. These small businesses could be tourism operators, growers and exporters of fresh produce or businesses reliant on imports. The type of hardship assistance offered may include: • A deferral of scheduled loan repayments; • Waiving fees and charges; • Temporary interest only periods to assist with cashflow; and • Debt consolidation to help make repayments more manageable For small business customers affected by COVID-19, please contact hardship assistance team directly on 1800 620 639 to find out if you are eligible for assistance. For the complete information on the Lender’s Media Release, click here. Latitude For clients that needs help as a result of COVID-19 may reduce monthly payments and reduced interest rates on on Credit Cards, Personal loans and Motor loans. Customers can complete the hardship assistance online using this form. For more information on how they can help, click here or call on 1800 220 718. Liberty Liberty has support measures tailored to meet customers individual needs and circumstances. For customers impacted by COVID-19, some options may include:

The best way to discuss individual circumstances is by calling on 13 11 33 or emailing help@liberty.com.au. Customers can also direct message us via our Facebook page. For more information, click here. Mortage Mart These are the latest numbers for clients needing to seek genuine Hardship Assistance from current funding lines: Origin 1300 224 656 La Trobe 1800 620 639 | Email is hardshipassist@latrobefinancial.com.au Pepper 1800 356 383 | Email is assist@pepper.com.au Advantedge 1300 155 426 Previous funding line contact numbers are: Resimac 1300 793 741 Firstmac 13 12 20 ING 1300 349 166" MyState MyState’s new measures to support customers who may be experiencing financial hardship due to COVID-19, include: 1. Home loan, personal loan or commercial loan customers can defer their payments for a period of up to six months with a check in at 3 months. 2. Allowing early access to Christmas Accounts without penalty. 2. Raising the maximum threshold on MyState’s high interest Bonus Saver Accounts from $150,000 to $250,000. 4. Allowing customers to redraw any amount (from $1) on home and personal loans, with fee- free redraws in-branch or through the Customer Care team as well as online, which has always been free. For full information on relief measure and to submit application, click here. Customer Care Team 138 001. P&N Bank For P&N Bank customers affected by the current COVID19 situation, and you are unable to repay your home loan as a result. All eligible members can apply for a repayment pause on their home loan for up to 6 months (subject to review at 3 months). This applies to both owner-occupied and investment loans for principal & interest or interest only repayment terms. Interest will be capitalised during the repayment pause. After the payment pause, scheduled minimum monthly repayments will need to be increased to repay the loan within the original repayment term. Customers who require repayment assistance, complete this form. For more information on the bank’s financial relief package, click here or call on 13 25 77. St George St. George home loan customers that are impacted of the pandemic may:

Repayment relief for small business customers: Eligible St.George small business customers who need help to manage their cash flow can defer principal and interest payments1 of business term loans (excluding credit cards, overdrafts, cashflow/invoice/trade finance, commercial bills), Business Auto, equipment finance facilities and equipment loans for six months.** For more information on the bank’s small business customers relief measures, click here. Teachers Mutual Teachers Mutual assistance packages are outline below: The assistance packages are outlined below. For Home Loans • For variable rate home loan, may be able to reduce the amount of minimum monthly repayment and retain the same loan term. • If paying more than your minimum monthly repayments, may have funds available to redraw, can use those funds to make the minimum monthly repayments. • If have funds available in your offset account, can use those funds to make the minimum monthly repayments. If the above options are not available, please contact to discuss whether eligible for a three-month deferral. There will be no impact to CCR reporting on loans that have agreed repayment pause arrangements. Direct number 1800 862 265 is or alternative General call centre number is 13 12 21 who will direct the call to the dedicated Financial Hardship team. For complete assistance package information, click here. Think Tank Think Tank have a range of measures are available from restructuring loans, releasing equity, altering terms and repayment arrangements from P&I to Int only, to deferrals. All customer enquiries should be directed to help@thinktank.net.au. Clients can complete the financial hardship assistance enquiry form. Here is a downloadable list of Australian Bank’s Financial Hardship team that you can contact on the web or on the phone. With the current situation of the Covid-19 pandemic, Get Smart Financial is here to help and support clients. If you’re dealing with the impact of the Covid-19 pandemic there are practical ways your bank can help, and could include; deferring loan payments, waiving fees and charges, helping with debt consolidation, etc. We have listed below just some bank’s relief package measures to address customers affected by Covid-19, as well as some useful links 👉 https://mailchi.mp/1ea96a054570/available-financial-hardship-packages-for-covid-19 If you have any concerns please do reach out to us by booking in time through our book me link, phone or email, we are here to support our clients at this critical time and will do all we can. BOOK ME 👉 https://getsmartfinancial.youcanbook.me/ #newsflash#cashratereduction#gettourfinanceinorder #save#getsmartfinancial#financeteam#mortgagebrokermelbourne#mortgagebrokeraustralia #weloveourclients#winningteam🏆 #inspiration#propertyfinance #finance  In the last few weeks I have been having quite a few conversations with clients around interest rates and how to save more money on your lending, but also around contingencies, insurances, and the overall economic climate - particularly now we are confronted with the potential fall out of the COVID-19 pandemic. Notwithstanding health and well-being as our utmost priority, there are a few other things to think about to help at least ease your mind and financial situation amidst this global crisis. Keep safe everybody, and as always, reach out if you would like to discuss further. BOOK A MEETING WITH RACHAEL: https://getsmartfinancial.youcanbook.me/ #getsmartfinancial#financeteam#mortgagebrokermelbourne#mortgagebrokeraustralia#weloveourclients#winningteam🏆 #inspiration #propertyfinance #finance#lending #covid19 #coronavirus#lenderaustralia  “Here’s to strong women. May we know them. May we be them. May we raise them.” – Unknown

“Nothing can dim the light which shines from within.” – Maya Angelou "Nothing in life is to be feared; it is only to be understood. Now is the time to understand more so that we may fear less" - Marie Curie #getsmartfinancial #empowerment#financeaustralia#womeninfinance  Time to review your home loan rate? You bet!

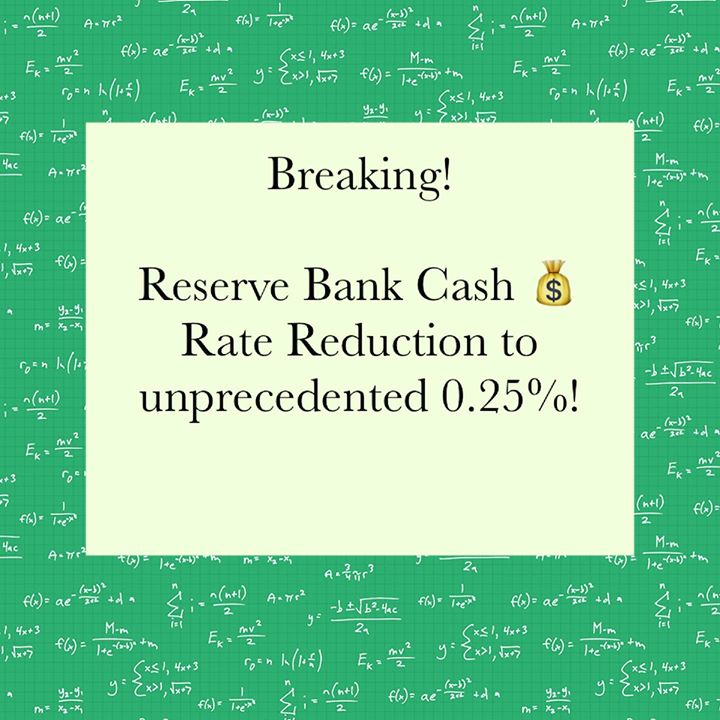

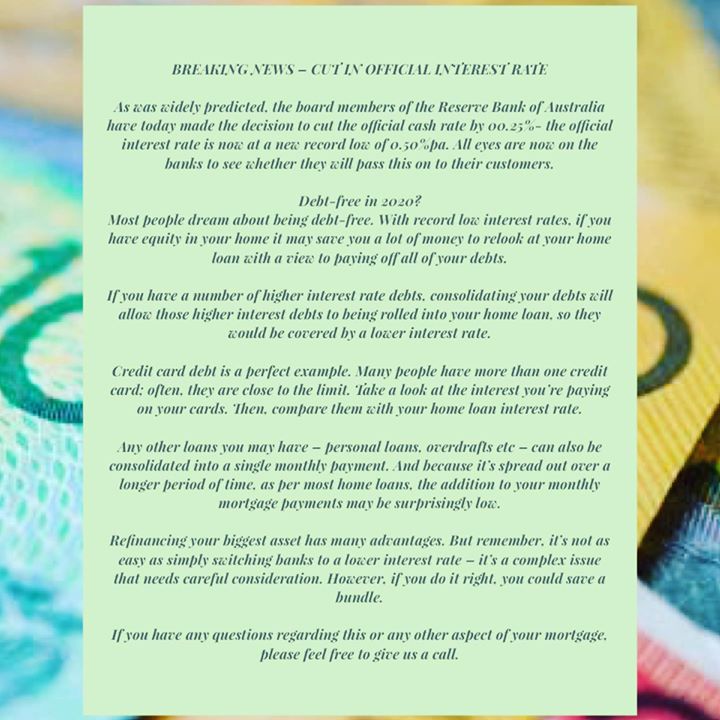

Money is cheap and this is absolutely the time to see how much you can save, and how you can pay down that debt faster, and we’ll do all the hard work for you at no cost to you! #reservebankofaustralia#cashrate#cashratereduction#savemoney#betterhomeloan #getsmartfinancial#financeteam#mortgagebrokermelbourne#mortgagebrokeraustralia #weloveourclients#winningteam🏆 #inspiration #propertyfinance#finance As was widely predicted, the board members of the Reserve Bank of Australia have today made the decision to cut the official cash rate by 0.25%. The official interest rate is now at a new record low of 0.50% pa. All eyes are now on the banks to see whether they will pass this on to their customers. Debt-free in 2020? Most people dream about being debt-free. With record low interest rates, if you have equity in your home it may save you a lot of money to relook at your home loan with a view to paying off all of your debts. If you have a number of higher interest rate debts, consolidating your debts will allow those higher interest debts to being rolled into your home loan, so they would be covered by a lower interest rate. Credit card debt is a perfect example. Many people have more than one credit card; often, they are close to the limit. Take a look at the interest you’re paying on your cards. Then, compare them with your home loan interest rate. Any other loans you may have – personal loans, overdrafts etc – can also be consolidated into a single monthly payment. And because it’s spread out over a longer period of time, as per most home loans, the addition to your monthly mortgage payments may be surprisingly low. Refinancing your biggest asset has many advantages. But remember, it’s not as easy as simply switching banks to a lower interest rate – it’s a complex issue that needs careful consideration. However, if you do it right, you could save a bundle. If you have any questions regarding this or any other aspect of your mortgage, please feel free to give us a call. #getsmartfinancial#financeteam#mortgagebrokermelbourne#mortgagebrokeraustralia #weloveourclients#winningteam🏆 #inspiration #propertyfinance#finance   NO CHANGE TO INTEREST RATES

There was rumour of a possible interest rate cut this month, but in the end the RBA chose to keep the official cash rate on hold. It remains at the record low of 1.5%pa. Experts continue to predict a cut at some stage this year. Last month we explained lenders mortgage insurance (If your deposit is less than 20% of the value of the home you will be required to take out lenders mortgage insurance, which protects the lender if you are unable to make home loan repayments). This month, we focus on another form of Mortgage Protection Insurance. Mortgage Protection Insurance Mortgage Protection Insurance (MPI) is a product that, in effect, insures you in the event that something should prevent you from meeting your commitments. If you become ill, suffer an accident etc. There are many variations offered and it is something to consider particularly if you have a family/ dependents. MPI varies from lender to lender. Basically, it involves a one-off payment towards your home loan if you die or will cover most or all of your monthly repayments if you are unable to work due to a series illness or injury (up to a set amount of months). As with most insurance, your eligibility takes into account whether a diagnosis has been make in the 12 months before you purchased the policy. It also covers monthly repayments if you become involuntarily unemployed. However, it does not apply if you quit your full time job, or if you are employed in a permanent part-time, casual, contract, or temporary capacity for less than 20 hours per week or you are self-employed and working less than 20 hours per week. Is it expensive? The exact cost of mortgage protection insurance will depend on:

Do you need Mortgage Protection Insurance? That depends on your personal circumstances. As usual, we are here to help – give us a call and we can discuss your options. Until next month,  Reserve Bank leaves interest rates on hold

As expected, the RBA Board has decided to keep the official cash rate on hold at the record low of 1.5%. Commentators expect this will continue, with the possibility of another cut before the end of the year. If this happens, conditions will be even more favourable for people who are saving up for their first home. Lenders mortgage insurance If you’re a first time homebuyer or an investor, it’s possible the deposit you have is less than 20% of the value of the home you want to buy. If this is the case, you’ll most likely need lenders mortgage insurance. It’s important to realise that lenders mortgage insurance benefit the lender, not you - it protects them if you are unable to make home loan repayments. The benefit of lenders mortgage to you is gives you the option to buy a home sooner, rather than later. However, it’s also important to know that this will add a further expense. The cost of lenders mortgage insurance depends on your loan – the larger the loan and the smaller your deposit, the more you’ll pay on insurance. Other factors (depending on the lender) may include whether you are employed full time or casually, and whether it’s your home or an investment property. How to avoid paying lenders mortgage insurance As the cost of lenders mortgage insurance can be more than you budgeted for, you’ll need to consider the following:

It’s best to know upfront whether or not you need lenders mortgage insurance. That’s where we can help – give us a call and we’ll help you navigate the home loan application process. Until next month,  Is the key to saving a home deposit as simple as giving up smashed avo toast for breakfast? Well not quite, but spending less does make a difference. On top of a budget, a savings plan and strategies such as a high-interest savings account, an effective way to save is to reduce or eliminate expenses. Start by understanding your spend It can be easy to lose track of how you’re spending money, especially due to cashless payments and credit cards. Many online banking systems include tools to categorise debits and make a budget – take advantage of them. Or download an app that helps you track your personal expenses on the go, like ASIC’s TrackMySPEND. Find savings in the essentials Some costs can’t be avoided – but many everyday expenses can be reduced. For example you could:

Make sure you’re paying off debts or credit cards completely each month or as much as possible, to avoid the added expense of paying interest. Reduce common overspending If you spend excessively on things like buying clothes, going out or expensive hobbies, it may be unrealistic to cut the expense entirely. Set a weekly or monthly limit and reduce that limit over time. A survey of more than 1000 Australians showed that 73 per cent have a problem with overspending. In particular, people tend to go overboard Christmas rolls around. To reduce gift expenses, be like Santa: make a list (and a budget). Buy only planned items within your allocated budget – then stop! Ask your family for support; it’s easier to put a cap on gift values if everyone else does too. Another common way Aussies overspend is on holidays. CommBank research has shown that a third of holidaymakers spent more on their trip than planned. Do your research and set a daily budget. Costs that could be eliminated Look for opportunities to eliminate costs. Cancel unused services. Update your internet or mobile plans if you’re always paying for excess data. Ask yourself: are you really using that gym membership? Are you getting value from your subscriptions? Remember, every wasted dollar is money you could be spending on your own home. edit.  Friends, throwing the box wide open this morning, and calling a spade a spade, and on an important matter which a number of clients have emailed me about over the weekend. There was an article published over the weekend by all the major publications, titled "If you have extra money in your mortgage, get it out now!" which has created a little panic, and unnecessarily so.... I want to put your mind at ease, and let you know, you can save the panic for more important things of impending emergency, such as being chased by a shark, or a lack of coffee in the cupboard, either of these qualify for hitting the emergency button. This kind of publication is scare mongering, putting the wind up people like the revelation is something new and imminent, which it really is not. To be clear, all contracts disclose that the bank can make changes to the limit, and repayment, and due dates of repayments, etc etc, to ensure that they comply with the contacted term, and there is not an impending and imminent cancellation of your savings sitting in your home loan or your offset account about to occur that is going to effect every home buyer in the country. In fact, if a bank wanted to, they could sweep funds from any account that you have with them, and dump it into your loan if the loan is out of order, and the current status and the bank failing to take action would mean they failed to keep their contractual obligations, and you had failed to meet yours! This, is not anything new either, and has been happening for well over 30 years. It is not something that occurs very often at all however, as it is not something the banks like to do.... really bad PR! But, if you were at risk of foreclosure on your home, and the bank could see that they could help you protect your home with savings you had sitting in another account, they will try to protect you from yourself, if you hadn't used the funds already to avoid that foreclosure. My advice? Let it go, it’s always been like this, and there is no point to this article other than to create panic. And, if you want to talk about it further with me, to discuss risk mitigation, call me, let's discuss, or even better, let's discuss over coffee, because coming to the realisation that there is no concern is even better with coffee, refer paragraph 2! |

AuthorRachael Bland – Founder & CEO Archives

February 2024

Categories

All

|

RSS Feed

RSS Feed

|

Privacy | Credit Guide | FAQs | Calculators

T: 0421 73 88 30 | E: rachael@getsmartfinancial.net.au Credit Representative Number: 427013 | Australian Credit Licence Number: 391237 | MFAA Accredited Credit Advisor 150638 | Copyright © 2019 Get Smart Results Pty Ltd |

Website by Mint Creative Circle

|