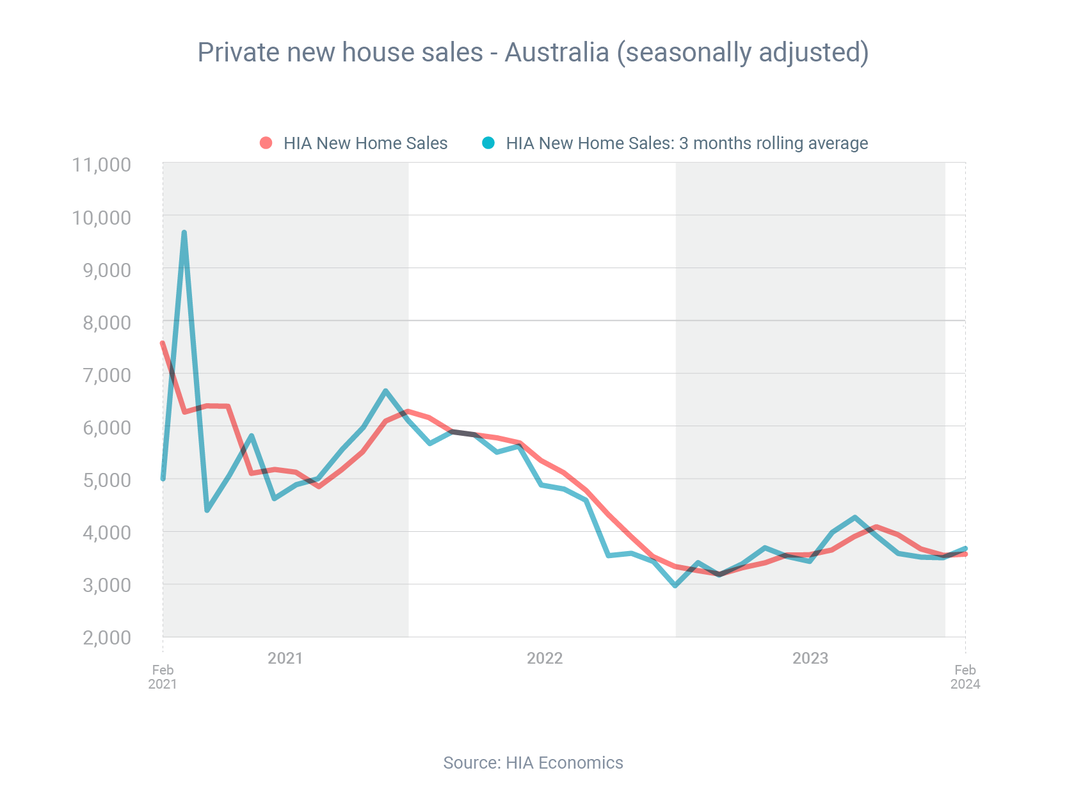

Australians purchased 5.3% more new homes in February than the month before, according to the Housing Industry Association (HIA). However, HIA chief economist Tim Reardon said this increase was off a “very low” base. Based on the number of new homes being approved for construction and purchased, he forecast there would be a decade-low amount of homebuilding activity in 2024, despite the pent-up demand for housing.  Nevertheless, banks are still keen to lend to Australians who want to build a new home or renovate an existing one. To finance your project, you’ll need a construction loan (rather than a regular home loan). Here’s how construction loans work:

First home buyers are able to enter the market a little faster than a year ago, new research has found. At a national level in February, it took 4 years 9 months for a first home buyer to save a 20% deposit on an entry-level house, compared to 4 years 11 months the year before. For an entry-level unit, the time to save a deposit was 3 years 5 months – one month faster than the year before.  Domain classified an entry-level property as one ranked at the 25th price percentile (with the 1st percentile being the cheapest home and the 100th being the dearest). Domain's calculations assumed that first home buyers were a couple aged between 25-34, earning an average salary for someone their age.

The reason that first home buyers are now able to save a deposit more quickly is not because property prices have fallen over the past year – because they've actually increased. Rather, it's because earnings power (through a combination of higher wages and higher savings account interest rates) has grown faster than property prices.  New research by the e61 Institute and PropTrack has revealed there's been a significant increase in relative stamp duty costs in recent decades. Back in the early 1980s, buyers in Sydney, Melbourne, Brisbane and Adelaide needed to do about one month's work to cover the cost of stamp duty, assuming they purchased a median-priced property and earned the average post-tax income. But as of 2023, it takes about six months’ work in Sydney and Melbourne, five in Adelaide and four in Brisbane. Last year, almost all buyers faced a stamp duty rate equivalent to at least 3% of the sale price, while, in the early 1990s, almost all buyers paid less than this amount.  PropTrack senior economist Angus Moore said the two reasons stamp duty had become relatively more expensive were because property prices had grown faster than incomes and state governments had allowed ‘bracket creep’ to occur with stamp duty tax brackets.

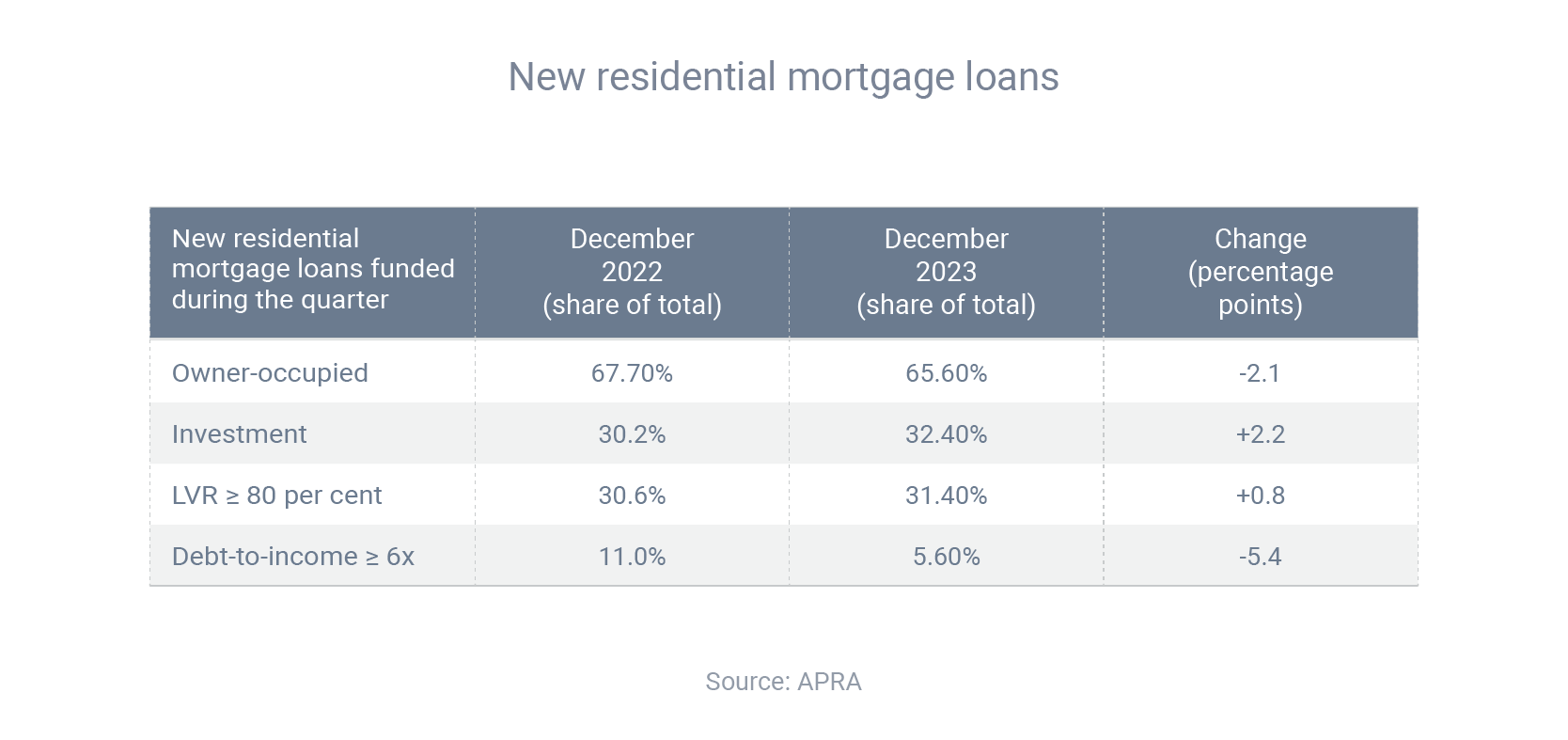

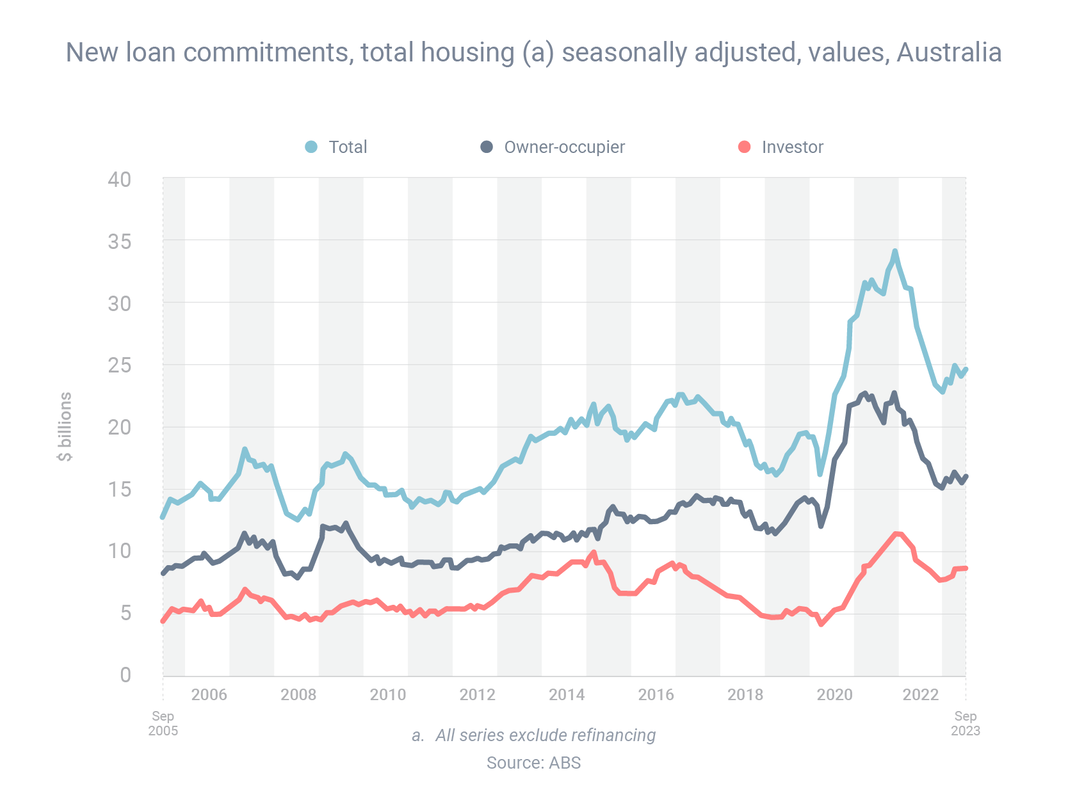

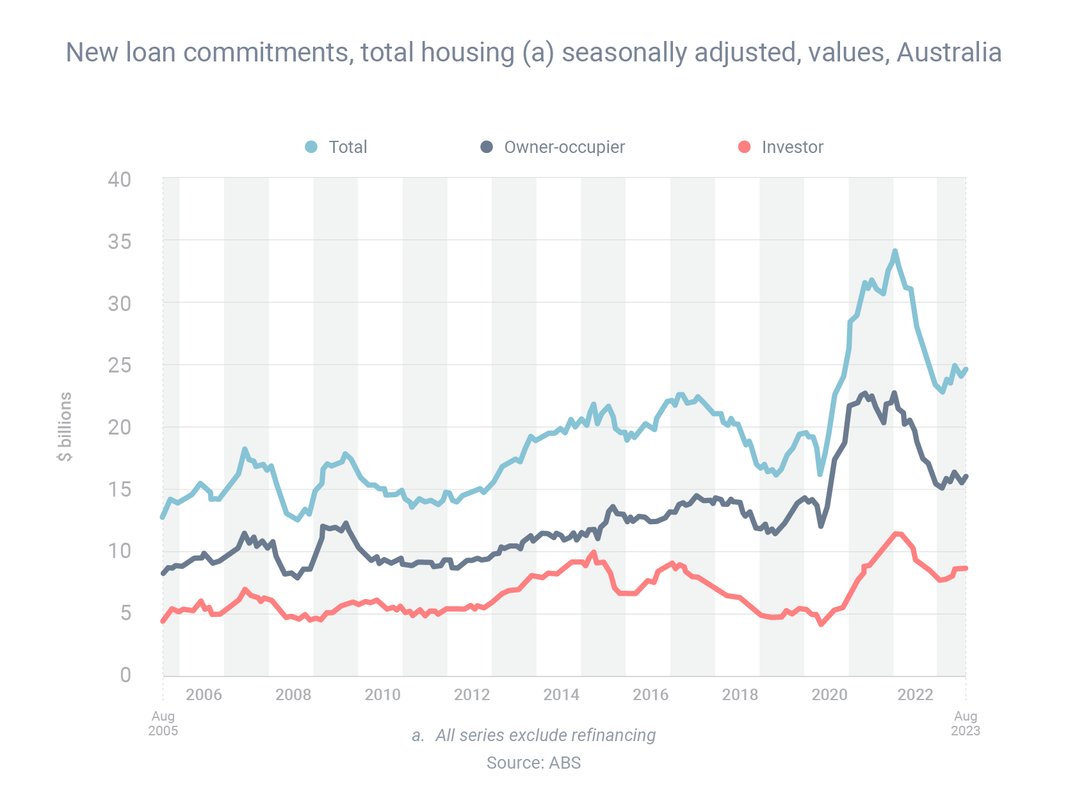

“Bracket creep happens, firstly, because the price brackets have been updated only infrequently and, secondly, because home prices have grown, often substantially, since the brackets were last set,” he said. “That means more properties have moved up the brackets and are now paying higher rates of stamp duty.”  The latest tranche of home loans data from the banking regulator, APRA, has revealed three interesting shifts in the mortgage market over the past year. First, there's been a meaningful rise in investor activity during that time. During the December 2022 quarter, 30.2% of new loans were for investment purposes; but in the December 2023 quarter, the share increased to 32.4%. There's been a corresponding decline in owner-occupier activity, which fell from 67.7% to 65.6%.  Second, there's been a sharp decline in borrowing with a debt-to-income of 6 or greater (e.g. someone on a $100,000 salary borrowing $600,000 or more). This fell from a 11.0% share of new loans in December 2022 to only 5.6% in December 2023.

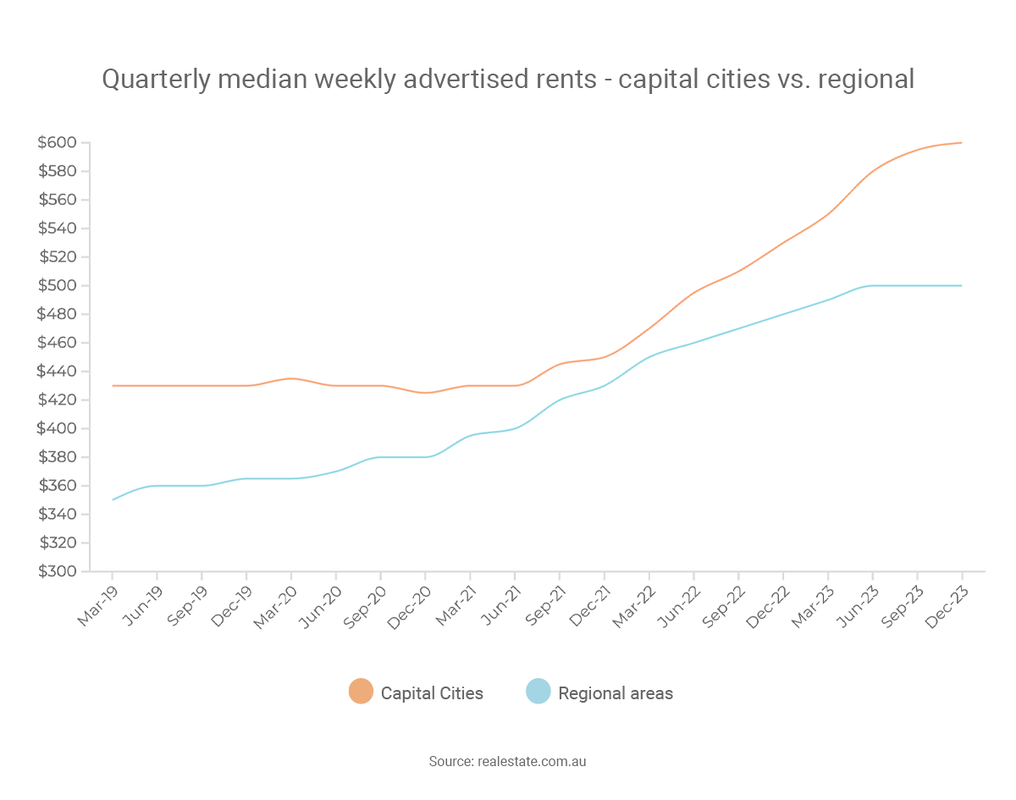

Finally, the share of borrowing with a loan-to-value ratio of 80% or higher has actually increased, from 30.6% of new loans in December 2022 to 31.4% in December 2023. Whether you’re an owner-occupier or investor, I can advise you about your borrowing power and help you get a great home loan.  Rents have increased in most capital cities over the past year and are likely to continue rising throughout 2024, according to a leading property data expert. Between the December quarters of 2022 and 2023, the median rent on realestate.com.au rose 11.5%. That included double-digit gains in Perth (20.0%), Melbourne (18.3%), Sydney (16.7%) and Adelaide (12.5%), as well as increases in Brisbane (9.1%) and Darwin (1.7%). By contrast, rents stagnated in Canberra (0.0%) and declined in Hobart (-4.8%). During the same period, the vacancy rate fell from 1.3% to just 1.1%. With rents growing and vacancies falling, this is potentially a good time to be a property investor.  PropTrack's director of economic research, Cameron Kusher, forecast that the “tough rental market conditions” would continue.

“We expect supply to remain tight and demand to stay strong, likely pushing rents higher,” he said. “Lending to investors trended higher over 2023, indicating that investors are returning to the housing market. However, many investors continued to sell, resulting in a relatively small pool of rental properties being available for the large number of people seeking accommodation. The rapid increase in Australia’s population exacerbated rental market challenges, as most people migrating to Australia become renters.”  A significant number of borrowers are unclear about lender’s mortgage insurance (LMI), according to a recent survey of mortgage brokers by LMI provider Helia.

The survey found that 85% of broker respondents think LMI can benefit buyers who want to get into the market earlier, while 70% believe it can also help renters who want to transition into ownership. However, 50% of respondents feel borrowers generally don't properly understand LMI. LMI is a form of insurance that protects the lender in case the borrower defaults on the mortgage and the lender can't recover the loan from selling the home. The premium varies, depending on the size, type and location of the property. Lenders generally insist borrowers take out LMI if they want to buy a property with less than a 20% deposit – although, for some professions, such as doctors and lawyers, it’s possible to buy a property with a smaller deposit without paying LMI. The upside to using LMI is you can enter the market with a smaller deposit; the downside is the cost. I’d be happy to discuss both the potential benefits and costs, so you can make an informed decision about whether LMI is right for your personal situation.  There's been a significant increase in first home buyer activity over the past year, based on the latest data from the Australian Bureau of Statistics. There were a total of 9,491 owner-occupier first home buyer mortgages issued across Australia in December 2023, which was 12.9% higher than the year before. First home buyer activity rose in six of the eight states and territories, with Queensland and Tasmania being the exceptions to the rule.  While it can be challenging to buy your first home, this data shows it’s not impossible. Here are four tips to get on the property ladder:

Six things every woman should know about their financial success on International Women’s Day Planning to succeed is integral, you don’t need to be buying a property to speak with a mortgage broker, it could be part of your plan in years to come, and they can be part of your success planning Knowing where your money goes each month, is integral… there are so many cheap, or free money management tools out there, so start tracking, work out where you can improve your cash flow, and move faster towards your savings / investment / home ownership goals The impact of maternity leave on your retirement strategy in years to come can be enormous. Thinking about how you might counter this impact, through additional super contributions, a more aggressive debt reduction, or savings plan, or having an agreement with your partner that during that time away from the workforce you will supplement your super with additional contributions to not leave you behind in later years, is important to forward plan for. Delegating our chores around the home, so you can focus on your work, career and family, and remain hyper focussed on the things you value, is key where you have big goals - contrary to popular belief, you don’t need to do it all! Assuming you cannot buy a home, without consulting a mortgage broker, would be a big mistake. There are a lot of misconceptions in the community, and asking questions, will help you get to where you want to go faster. Having boundaries to ensure your body, and mind are as best as you can be, is integral to success. Remember, you have to put your face mask on first, before you can help anyone else, and you need to be in the right place, to be a great boss, staff member, parent or friend. Running yourself into the ground, never helped anyone!  Many economists believe the Reserve Bank will start cutting interest rates in the final quarter of 2024. So if you're thinking about entering the market, should you buy now or wait for those potential rate cuts to occur? To answer that question, it can be helpful to consult long-term data. During the decade to January 2024, Australia's median property rose 80.1%, according to PropTrack. Prices rose faster in the combined regions than the combined capital cities (92.5% vs 75.7%), while house growth exceeded unit growth (89.4% v 44.4%). But the general trend for all these categories was the same – up. Domain's chief of research & economics, Nicola Powell, believes buyers should take a longer-term view and not get too hung up about how the market is currently performing.  “When you’re purchasing a property, it’s for a long-term investment and you are going to ride multiple property cycles, and that’s how you build financial wealth. So if I would give any advice, it would be to buy when it’s right for you. Housing markets are complex and often impossible to predict.”

Ultimately, the question or whether to buy now depends on your personal situation and goals. For some, now will be the right time; for others, it will be better to wait. I'm happy to have a chat and crunch some numbers for you, so I can present personalised loan options for your situation.  Becoming a better budgeter can help you save more, invest more and get ahead on your home loan.

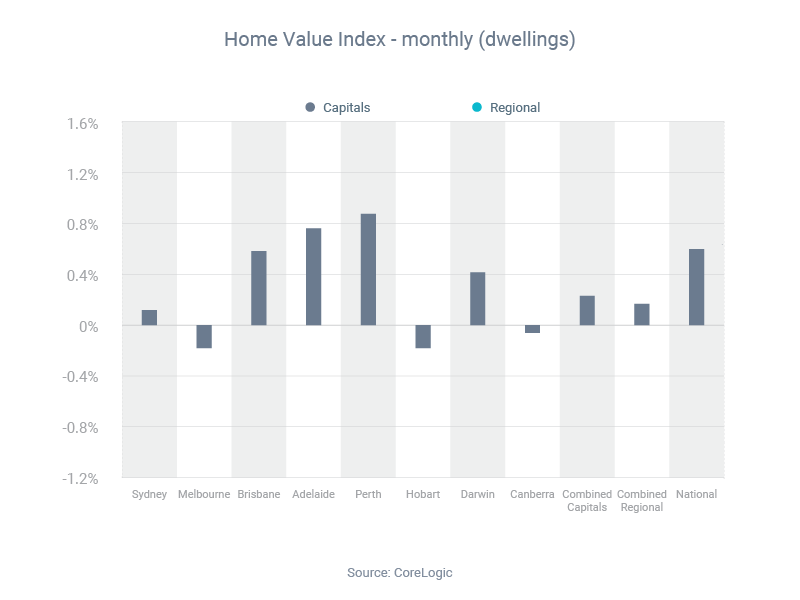

To stay on top of your finances, there are two broad approaches you can take. The first is to plan how much you’ll spend on each category (groceries, entertainment, etc) each month. If you stick to your budget, you’ll know in advance how much you’ll save. The second approach is to throw out the budget and focus on saving instead: Decide how much money you want to save each month Set up an auto-transfer to move this amount of money from a transaction account to a savings account whenever your salary gets paid Spend whatever is left in the transaction account, however and whenever you like The first approach suits people who want to pay close attention to their money, while the second is for people who want to ‘set and forget’ their savings. Whichever approach you take, a good place to begin is to review your last 12 months of expenses, to see how much you’re spending and on what things. You can use that information to identify areas of wastage and set savings targets.  Australia's median property price reached a record $757,746 at the end of 2023, after another year of growth. The median price rose 3.0% during the pandemic year of 2020, surged 24.5% in 2021, contracted 4.9% in 2022 and then climbed another 8.1% in 2023, according to CoreLogic. The median price for the combined capitals ended 2023 at record levels, while the combined regions were just 1.5% off peak. December was the 11th consecutive month of price gains (see graph) – however, as CoreLogic research director Tim Lawless noted, it was also the smallest of those monthly gains, at 0.4%.  “After monthly growth in home values peaked in May at 1.3%, a rate hike in June and another in November, along with persistent cost of living pressures, worsening affordability challenges, rising advertised stock levels and low consumer sentiment, have progressively taken some heat out of the market through the second half of the year,” he said.

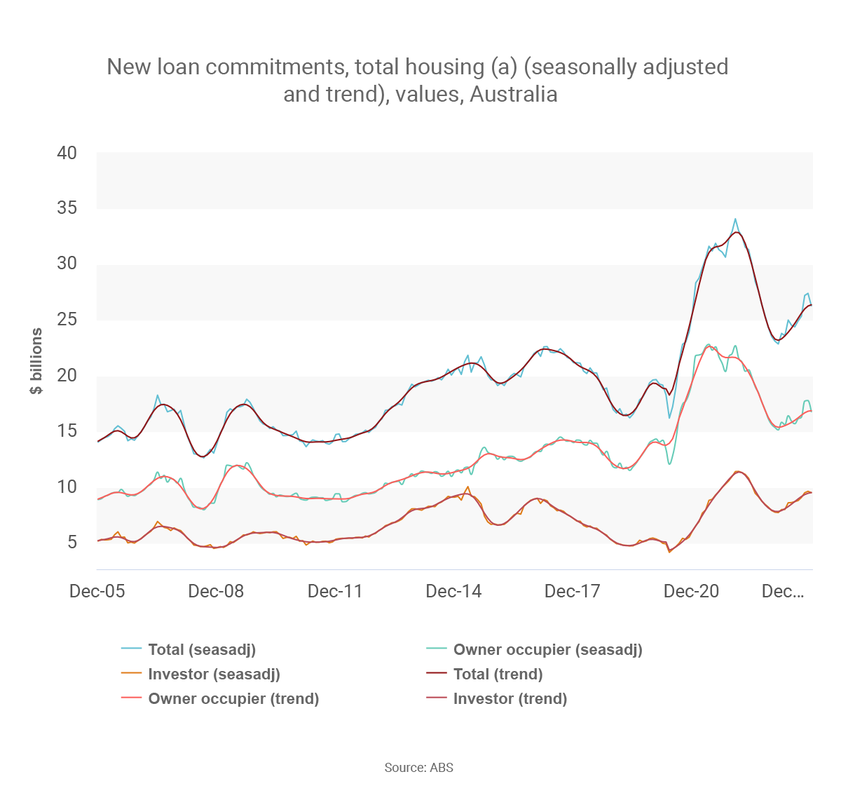

As interest rates move up and down, so does the average person's borrowing power. Borrowing power tended to decline in 2023 and is likely to change again in 2024 as rates evolve. The other point worth mentioning is that your borrowing power can vary significantly from lender to lender. The good news is that I can match you with a bank that wants to lend to someone with your situation.  Every state has recorded a rise in property investor borrowing over the past year, with Western Australia leading the way. Throughout Australia, investors took out $9.72 billion of home loans in November 2023, which was 18.0% higher than the year before, according to the most recent data from the Australian Bureau of Statistics. Looking at the individual states, the year-on-year increases in investor borrowing ranged from 3.5% in Victoria to 42.1% in Western Australia.  This strong increase in property investor activity might be because investors are enjoying a double wealth gain right now: during 2023, investors enjoyed increases in both the national median property price (by 8.1%) and national median rent (by 8.3%), according to CoreLogic.

One of the key things to remember with investor loans is that your outcomes can vary significantly from lender to lender. Depending on your financial position and the property you want to buy, different lenders will offer you different loan products, loan sizes and interest rates. As your broker, I will compare the market for you and shortlist lenders that suit someone with your specific scenario.  The Australian Taxation Office (ATO) has significantly increased its tax take, in part through a focus on large businesses.

Speaking before the Senate Economics Legislation Committee, ATO Commissioner Chris Jordan said the ATO's net collections in the 2022-23 financial year were $576 billion – up $60.6 billion on the previous year. “Rates of corporate tax compliance in Australia continue to set a very high bar for the rest of the world,” he said. “Since the Tax Avoidance Taskforce commenced in 2016, it has helped secure around $28 billion in additional tax revenue from multinational enterprises, large public and private businesses.” Commissioner Jordan said the ATO's decision to target the big end of town helped send a positive message to smaller businesses. “When the community sees large corporates doing the right thing, we know this has a positive influence on attitudes and behaviour to paying tax,” he said. “Small and medium businesses and individual taxpayers contribute significantly to our bottom line.” Commissioner Jordan also said the ATO wanted “to encourage a culture of paying tax on time and in full”, for businesses of all sizes.  Retail turnover has now increased for three consecutive months, but sales remain at low levels as consumers think twice before spending. Turnover rose 0.9% in September, after previously increasing 0.3% in August and 0.6% in July, according to the Australian Bureau of Statistics (ABS). “The warmer-than-usual start to spring lifted turnover at department stores, household goods and clothing retailers, with more spending on hardware, gardening, and clothing items. Also adding a boost to turnover in household goods retailing was the release of a new iPhone model and the introduction of the Climate Smart Energy Savers Rebate program in Queensland,” ABS Head of Retail Statistics Ben Dorber said.  However, he also said that “subdued spending for most of 2023 means that underlying growth in retail turnover remains historically low”.

Retail turnover in September was only 2.0% higher year-on-year. Looking at the different retail categories, the change in turnover was:

The Australian Taxation Office (ATO) has noticed a spike in businesses reporting but not remitting GST, ATO Deputy Commissioner Hector Thompson said in a speech to The Tax Institute's national GST conference.

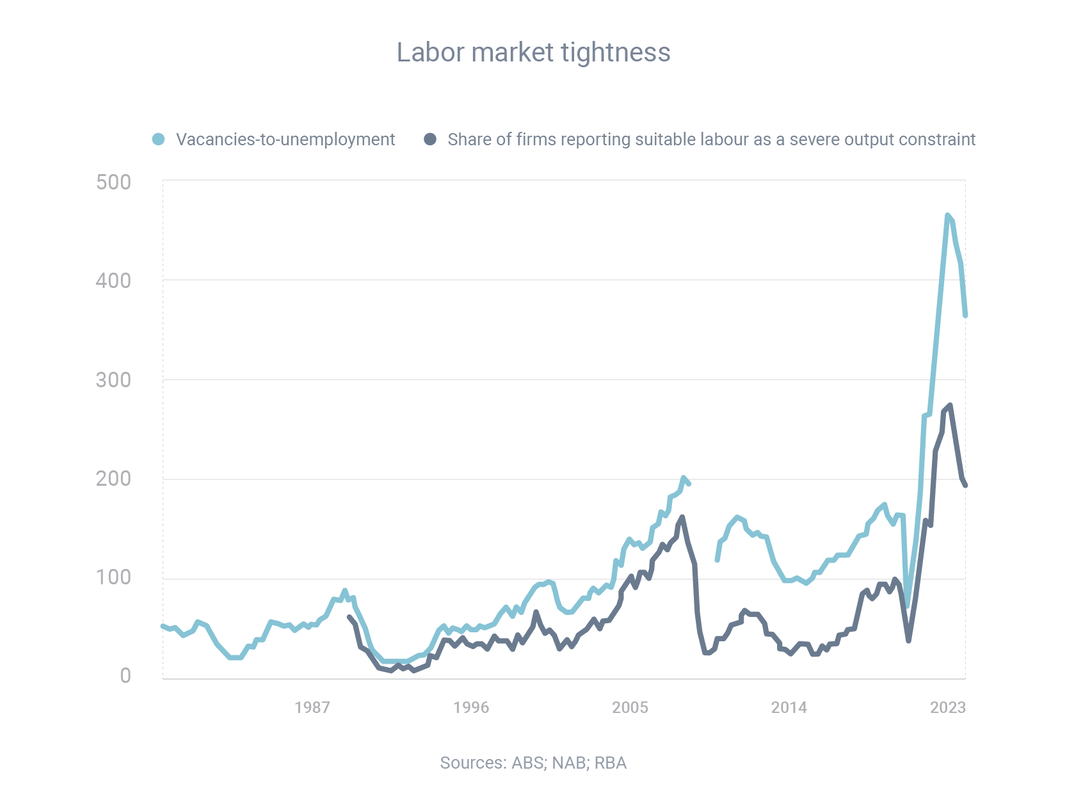

As a result, GST debt more than doubled in the three years to 30 June 2022. “While this increase in debt has been experienced across all taxes the ATO administers, GST debt is growing the fastest. We understand that recent times have been challenging and there will be more challenges ahead. However, reporting, but not remitting GST creates an uneven playing field for businesses that do remit the GST,” he said. Deputy Commissioner Thompson said the ATO was introducing a program to provide accountants with information about potential GST risks. “Over the next four years, we will undertake early intervention engagement activities with registered tax agents who may have clients that exhibit potential GST-related risks. The aim of the program is to educate and leverage agents’ relationships with their clients to positively influence their behaviours and ensure compliance with regulations,” he said. “We will deliver risk alerts to some tax agents providing a view of potential risks in their client base. The intention here is to encourage agents to review their processes and interactions with their clients, and take corrective action, where appropriate.”  Broad measures of labour underutilisation have increased over the course of the year as the economy has slowed, according to the latest Statement of Monetary Policy from the Reserve Bank of Australia (RBA). Nevertheless, the job market remains strong, which means the data is giving mixed signals:

As a result, the labour market remains tight and “finding suitable workers continues to be difficult” for businesses.

One interesting trend the RBA has observed is a change in the nature of how businesses are choosing to employ people. “Employment growth has increasingly been driven by part-time employment in recent months. This contrasts to patterns observed during the recovery from the pandemic, when full-time employment accounted for almost all employment growth. Relatedly, average hours worked have declined a little recently and are expected to remain a key margin of adjustment as labour demand eases further,” the RBA said.  NAB Monetary Policy Update: RBA to Hold Rates Until Late 2024, Cuts Expected in 2025

Key Points:

Softer Inflation Eases Pressure on RBA:

Outlook for Growth and Labor Market:

Risks and Uncertainties:

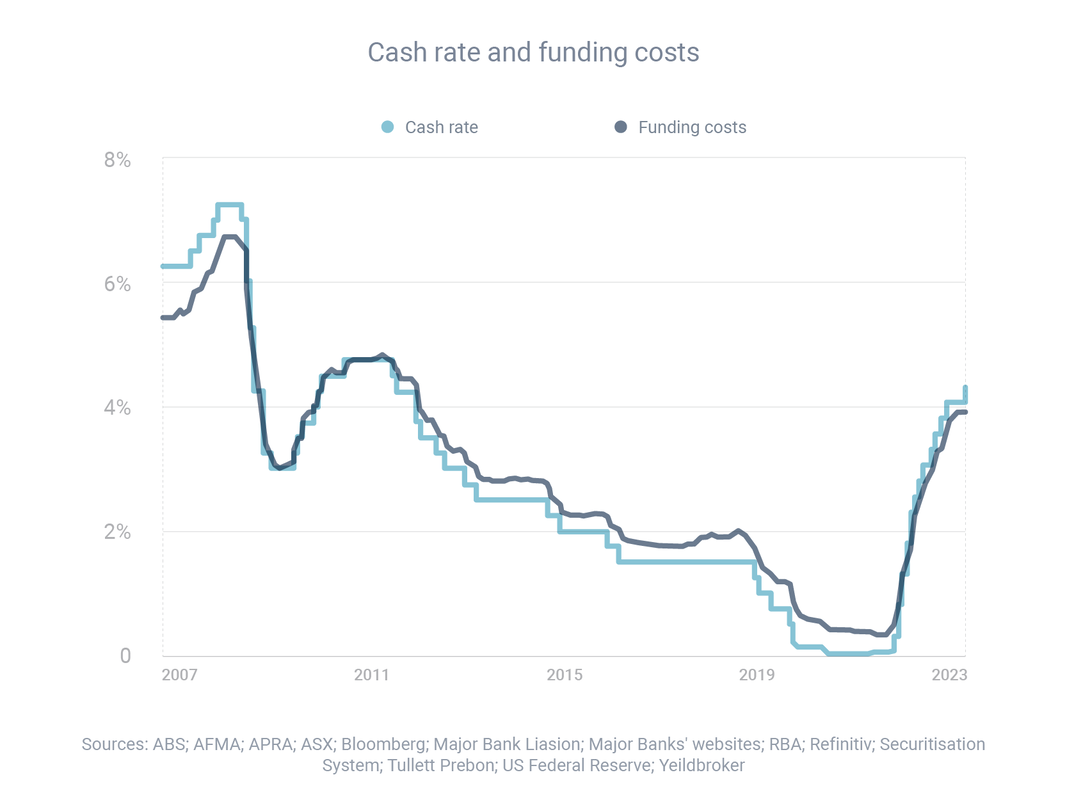

Overall, NAB's revised forecast suggests a period of stability in interest rates before potential cuts in late 2024, with the RBA focusing on balancing inflation and labor market concerns.  While interest rates have increased significantly over the past 18 months, this increase, thankfully, has been less than one might have expected, due to competition, according to the Reserve Bank. Between April 2022 and September 2023, the cash rate increased by 4.00 percentage points. However, banks increased their variable rates by, on average, only 3.32 points for owner-occupiers and 3.28 points for investors. This was due, in part, to “the effect of competition between lenders on variable-rate housing loans”.  Meanwhile, banks’ funding costs increased further between the June and September quarters, which is likely to lead to higher interest rates and more pain for households.

The increase in funding costs came “as banks replaced maturing bonds issued at much lower rates and average deposit rates increased”. Banks generally ‘buy’ funding on the wholesale market, add a margin and then on-sell this money to borrowers in the form of home loans (and other loans). So when banks' funding costs increase, they generally have little option but to increase rates as well.  A new report from CoreLogic has found that median property prices increased in 82.4% of local markets in the three months to October, based on a sample of 4,506 suburbs across Australia. That included price increases in 83.1% of house markets and 80.6% of unit markets. Focusing just on house markets, prices increased in:

CoreLogic's head of research, Eliza Owen, said many housing markets across the country were growing, despite high interest rates and weakening economic conditions.

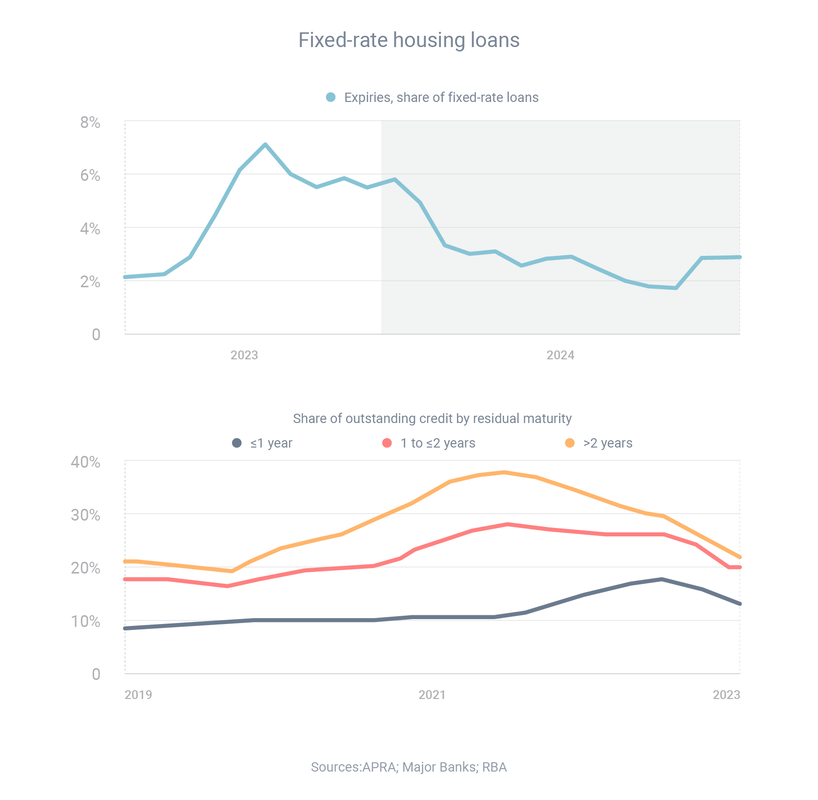

“It’s often noted that Australia is not ‘one housing market’ and we’re currently seeing increased diversity in capital city market performance,” she said. “That’s reflected in city-wide growth rates, the various levels of supply that’s available in some cities over others, and it’s reflected in the different suburbs we analyse in this report.”  The great transition of the mortgage market, from having a heavy share of fixed-rate loans to now being dominated by variable-rate loans, has gathered pace, according to Reserve Bank data. During 2020 and 2021, when interest rates fell to record-low levels, enormous numbers of borrowers took out two-year and three-year fixed loans at very low interest rates. Many of those loans then expired as rates started rising, meaning that many borrowers have been reverting from ultra-low fixed rates to significantly higher variable rates.  “The fixed-rate share of total outstanding housing credit declined to 22% in September, well below its peak of just under 40% at the start of 2022,” the Reserve Bank reported in its recent Statement of Monetary Policy.

Over recent months, the number of fixed loans that have expired have outweighed the number of new fixed loans that have been initiated, by a ratio of more than five to one. “Most of the remaining fixed-rate loans are expected to expire by the end of 2024,” according to the Reserve Bank.  There's been a big rise in home loans activity over the course of the year, with investors leading the way. Between February and September, the total volume of mortgage commitments rose 9.5% to $25.0 billion, according to the latest data from the Australian Bureau of Statistics. Owner-occupied borrowing climbed 6.1% to $16.1 billion, while investor borrowing jumped 16.0% to $9.0 billion.  Three other key facts:

The Australian Taxation office (ATO) has reminded taxpayers to lodge their taxes by the October 31 deadline or engage with a registered tax agent to avoid late lodgment penalties.

If you have simple tax affairs, you can lodge online, often in under 30 minutes, through the myGov portal. Most of the information you need will already be pre-filled – just check it's correct, add any additional income and claim your legal deductions. The ATO has also stressed the importance of making sure any claims you make for work-related expenses are accurate, which means you can't just automatically copy/paste the previous year's claims. “We want people to get their deductions right on the first go and claim what they are entitled to – nothing more, nothing less. We have a series of 40 occupation and industry-specific guides which you should have a look at,” ATO assistant commissioner Rob Thomson said. “It may be tempting to boost your refund by leaving out income or inflating your deductions – but remember, we have sophisticated data analytics that will pick up returns that look suspicious.”  A new report, from Housing Australia, has revealed that about one in three of all first home buyers in the 2022-23 financial year used the federal government’s Housing Guarantee Scheme (HGS) and its three different assistance programs.

Here’s what the typical participant looked like, according to Housing Australia:

Housing Australia has not only taken control of the HGS, but also the National Housing Infrastructure Facility, which provides loans and grants for critical infrastructure to unlock and accelerate new housing supply.  The latest Reserve Bank of Australia (RBA) data has shown the impact the RBA's cash rate rises have had on the mortgage market. The key is to compare average interest rates for all outstanding loans in April 2022 – the month before the first rate rise – and August 2023 – the most recent month for which we have data. During that time, the RBA increased the cash rate by 4.00 percentage points. Interest rates for outstanding loans have, on average, increased by less than that amount, in part because some loans were fixed at lower rates. For owner-occupied loans, rates have increased by an average of:

For investment loans, rates have increased by:

With lots of people coming off fixed rates right now, it’s no surprise that an enormous amount of refinancing is occurring, as borrowers look to switch to lower-rate loans. The latest Australian Bureau of Statistics (ABS) data has revealed that borrowers did $20.60 billion of refinancing in August – which was 3.9% lower than the month before but 12.4% higher than the year before. Meanwhile, the ABS also revealed that the value of all new home loan commitments in August was $24.82 billion, which was 2.2% higher than the month before. Owner-occupier borrowing rose 2.6% to $16.07 billion, while investor borrowing rose 1.6% to $8.75 billion. That said, home loan activity has fallen on a year-on-year basis:

The interest rate environment has changed a lot recently, and the level of competition in the mortgage market is fierce, so there are a lot of great refinancing deals available – including with quality smaller lenders you may be unfamiliar with.

|

AuthorRachael Bland – Founder & CEO Archives

February 2024

Categories

All

|

RSS Feed

RSS Feed

|

Privacy | Credit Guide | FAQs | Calculators

T: 0421 73 88 30 | E: rachael@getsmartfinancial.net.au Credit Representative Number: 427013 | Australian Credit Licence Number: 391237 | MFAA Accredited Credit Advisor 150638 | Copyright © 2019 Get Smart Results Pty Ltd |

Website by Mint Creative Circle

|